Introduction: The Nexus Between Age and Life Insurance

Term life insurance is often described as the most straightforward and cost-effective form of life insurance available. Unlike whole life insurance, which provides coverage for the entirety of an individual’s life and includes a cash-value component, term life insurance covers a specific period—typically 10, 20, or 30 years. However, the affordability of this financial instrument is heavily dictated by one primary factor: the age of the applicant. Understanding how term life insurance rates fluctuate by age is essential for any individual seeking to build a robust financial safety net for their loved ones.

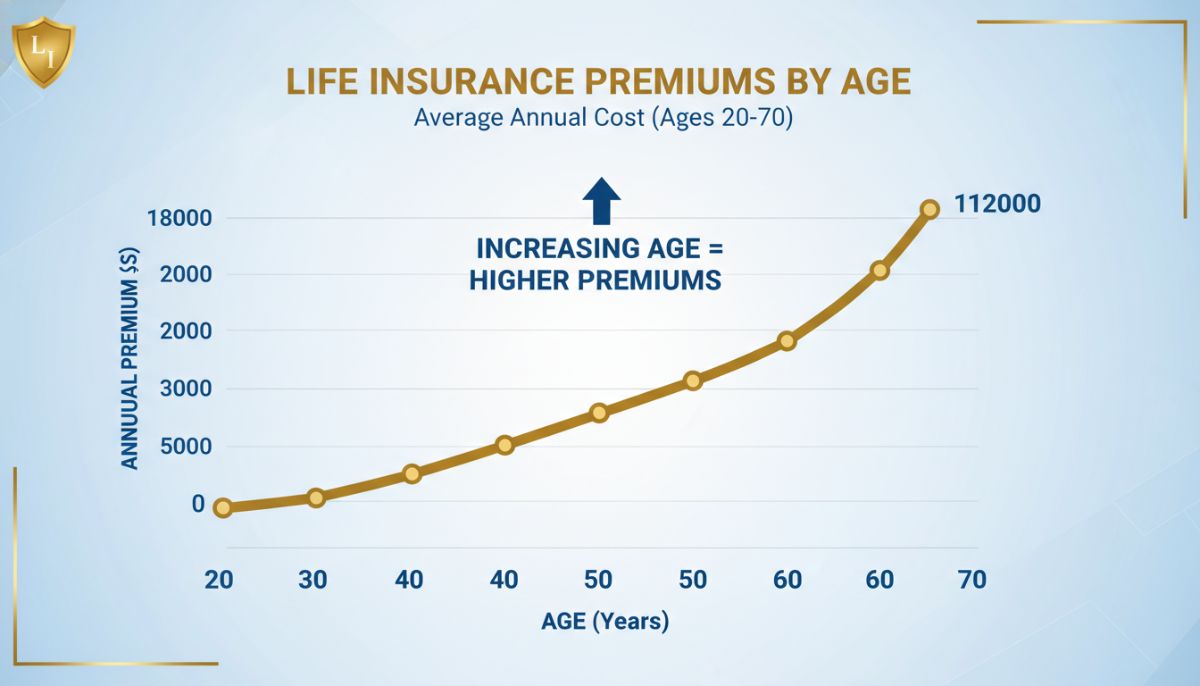

From an actuarial perspective, age is the most significant indicator of risk. As an applicant grows older, the statistical probability of mortality increases, prompting insurance companies to adjust premiums upward to compensate for the higher likelihood of a payout. In this guide, we will analyze the shifts in term life insurance rates across different life stages and discuss how strategic timing can save policyholders thousands of dollars over the duration of their coverage.

The Actuarial Logic: Why Age Matters

To understand term life insurance rates by age, one must first understand the concept of underwriting. Insurance companies use a process called mortality modeling to predict life expectancy. Younger individuals are statistically less likely to succumb to chronic illnesses or natural death within the term period. Consequently, they are classified as lower-risk assets. For every decade that passes, the risk profile changes significantly.

Typically, for every year you wait to purchase a policy, the premium increases by roughly 5% to 8% in your 30s and 40s, and as much as 10% to 12% once you cross the age of 50. This compounding effect means that delaying a purchase by even five years can result in a substantially higher total cost of ownership.

Term Life Insurance in Your 20s: The Golden Opportunity

In your 20s, life insurance is rarely a priority. Most individuals in this age group are focused on student loans, career entry, and social mobility. However, from a financial efficiency standpoint, the 20s are the optimal time to secure a policy.

At this stage, health is generally at its peak, and the absence of chronic conditions allows applicants to qualify for ‘Preferred Plus’ or ‘Super Preferred’ rate classes. A 20-year term policy with a $500,000 death benefit for a healthy 25-year-old can often cost less than a monthly subscription to a streaming service. By locking in these rates early, particularly through a level-term policy, the individual ensures that their premiums remain unchanged even if their health declines later in life.

The 30s: Balancing Family and Financial Protection

The 30s represent the most common decade for purchasing life insurance. This is the period when most individuals experience significant life milestones: marriage, purchasing a home, and starting a family. These milestones create a ‘need’ for insurance to cover mortgage debt and provide for dependents.

While rates in the 30s remain highly affordable, there is a visible uptick compared to the 20s. A 35-year-old might pay 20-30% more than they would have at 25. Nevertheless, the cost-to-benefit ratio remains excellent. It is during this decade that many opt for 30-year terms, ensuring that their children are reached adulthood and their mortgage is substantially paid down by the time the policy expires.

The 40s: The Turning Point in Premium Costs

As individuals enter their 40s, the underwriting process becomes more rigorous. This is often the decade where minor health issues—such as elevated cholesterol or high blood pressure—begin to manifest. These ‘lifestyle’ health markers can shift an applicant from a ‘Preferred’ category to a ‘Standard’ category, further inflating the cost beyond the base age-related increase.

For those in their 40s, the focus often shifts toward protecting their peak earning years. If a primary breadwinner passes away during this decade, the loss of future income can be devastating to a family’s long-term financial health. Despite the higher premiums, term life insurance remains a critical component of a mid-life financial strategy.

The 50s and 60s: High-Stakes Coverage

Once an applicant reaches the age of 50, the cost of term life insurance begins to accelerate rapidly. In many cases, a 50-year-old will pay double what a 30-year-old pays for the same amount of coverage. By this stage, insurers are looking closely at family medical history and the results of a required medical exam (unless a no-exam policy is chosen, which typically carries even higher premiums).

In the 60s, term life insurance is often used for specific purposes, such as covering the remaining years of a mortgage or providing liquidity for estate taxes. Some insurance companies limit the length of the terms available to older applicants; for example, a 65-year-old may not be eligible for a 30-year term policy, as the term would extend beyond the average life expectancy.

Factors That Influence Rates Alongside Age

While age is the primary driver of cost, it does not exist in a vacuum. To get an accurate picture of term life insurance rates, one must consider:

1. Gender: Statistically, women have longer life expectancies than men. As a result, women generally pay lower premiums than men of the same age.

2. Health Status and BMI: Your body mass index (BMI), history of tobacco use, and chronic conditions significantly impact your rating class.

3. Policy Length and Amount: Naturally, a 30-year term for $1 million will cost more than a 10-year term for $250,000.

4. Lifestyle Choices: High-risk hobbies (like skydiving) or dangerous occupations can lead to ‘flat extra’ charges added to your base rate.

Conclusion: Strategic Recommendations

The data is clear: term life insurance rates by age follow an inevitable upward trajectory. The most effective strategy for managing these costs is early intervention. By securing coverage as early as possible, you benefit from the lower risk profile associated with youth and health.

For those who have already entered their 40s or 50s without coverage, the best time to buy is today. Waiting further will only result in higher premiums and the potential for new health issues to complicate the underwriting process. Ultimately, term life insurance is not just an expense—it is a strategic purchase that provides peace of mind, ensuring that your family’s financial future is not left to chance regardless of when your time comes.