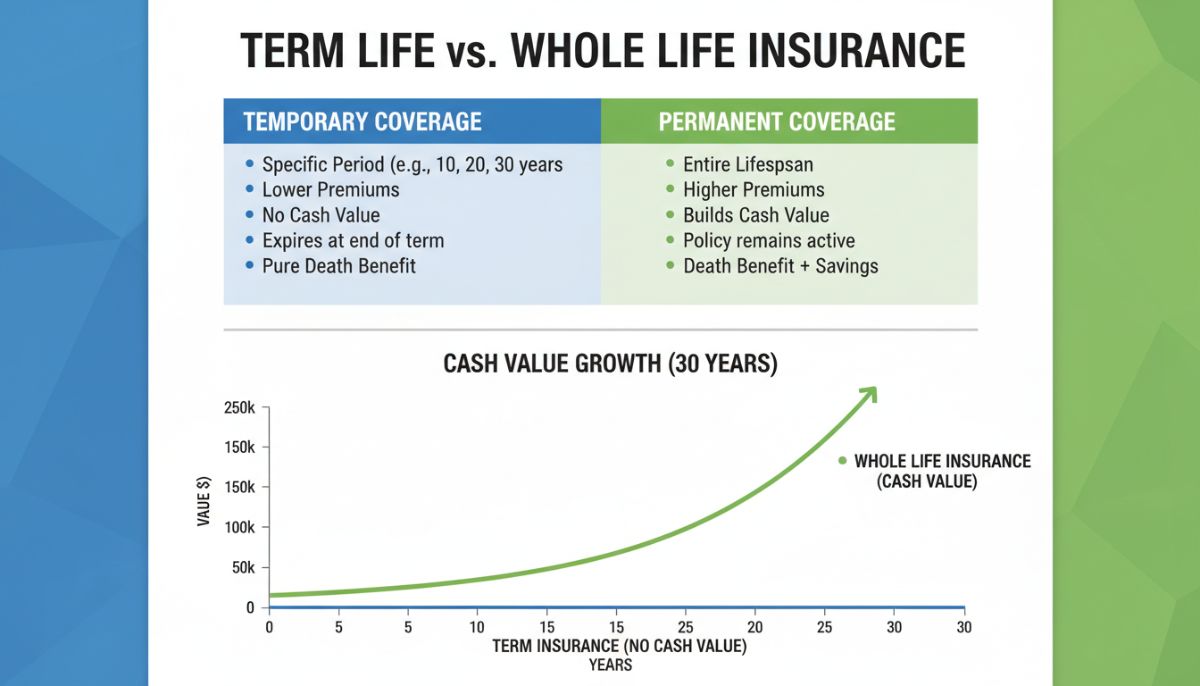

Introduction to Whole Life Insurance Cash Value

Whole life insurance is often characterized as more than just a death benefit; it is a complex financial instrument that combines permanent protection with a savings component known as cash value. Unlike term life insurance, which provides coverage for a specific period and carries no residual value, whole life insurance is designed to last the policyholder’s entire lifetime. The cash value component is the engine that drives the long-term utility of the policy, acting as a living benefit that the policyholder can utilize during their lifetime. Understanding how this value accumulates, the tax advantages it offers, and the methods for accessing it is essential for any individual seeking to integrate life insurance into a broader financial or estate plan.

The Mechanics of Cash Value Accumulation

When a policyholder pays a premium for a whole life insurance policy, the payment is not applied in its entirety to the death benefit. Instead, the insurance company allocates the premium into three distinct categories: the cost of insurance (mortality charges), administrative and overhead fees, and the cash value account. In the early years of a policy, a significant portion of the premium is directed toward the cost of insurance and the high upfront administrative costs, including commissions and underwriting. Consequently, cash value accumulation is typically slow during the first five to ten years.

As the policy matures, the portion of the premium required to cover the cost of insurance decreases relative to the total premium, and the cash value begins to grow more rapidly through a combination of premium contributions and guaranteed interest. Most whole life policies offer a contractually guaranteed rate of return on the cash value, ensuring that the account grows regardless of market volatility. This stability makes whole life insurance an attractive “safe money” asset class for conservative investors.

The Role of Dividends in Participating Policies

While the guaranteed interest rate provides a floor for growth, many whole life policies are “participating” policies issued by mutual insurance companies. In a participating policy, the policyholder is eligible to receive a share of the company’s profits in the form of dividends. Although dividends are never guaranteed, many major mutual insurers have a history of paying them consistently for over a century.

Dividends can be utilized in several ways: they can be taken as cash, used to reduce annual premium payments, or, most effectively, used to purchase “paid-up additions” (PUAs). Paid-up additions are essentially small increments of fully paid-up whole life insurance that have their own cash value and death benefit. By reinvesting dividends into PUAs, the policyholder creates a compounding effect that can significantly accelerate the growth of the cash value over time.

[IMAGE_PROMPT: A high-quality photo of a professional financial advisor pointing at a growth chart on a digital tablet in a modern office, explaining compounding interest to a client.]

Tax Advantages and the Internal Revenue Code

One of the most compelling reasons for the popularity of whole life insurance among high-net-worth individuals is its tax-favored status. Under current U.S. federal tax law (specifically Internal Revenue Code Section 72), the growth of cash value within a life insurance policy is tax-deferred. This means that as long as the funds remain within the policy, the policyholder does not owe annual income taxes on the interest or dividends earned.

Furthermore, the death benefit is generally received by beneficiaries free of federal income tax. If managed correctly, the cash value can also be accessed tax-free through a combination of basis withdrawals and policy loans. This triple tax advantage—tax-deferred growth, tax-free access, and a tax-free death benefit—positions whole life insurance as a powerful tool for tax-efficient wealth transfer and retirement planning.

Accessing Policy Liquidity: Loans and Withdrawals

The liquidity of a whole life policy is one of its primary “living benefits.” Policyholders can access their cash value through two main avenues: withdrawals and loans.

1. Policy Withdrawals

Withdrawals allow the policyholder to take cash out of the policy. Withdrawals are generally tax-free up to the “basis” (the total amount of premiums paid into the policy). However, withdrawals reduce the death benefit and the total cash value available for future growth. If a withdrawal exceeds the basis, the excess is taxed as ordinary income.

2. Policy Loans

Policy loans offer a unique way to access capital without triggering a tax event. When a policyholder takes a loan, they are technically borrowing money from the insurance company using the cash value as collateral. Because the cash value remains inside the policy, it continues to earn interest and dividends (though some companies may credit a lower interest rate on the portion of the cash value that is collateralized). The loan can be repaid at the policyholder’s discretion, or if unpaid, the balance is deducted from the death benefit upon the insured’s passing.

[IMAGE_PROMPT: A conceptual 3D illustration of a glass jar filling with gold coins, labeled ‘Cash Value Accumulation’, with a shield icon in the background protecting the wealth.]

Strategic Use Cases for Cash Value

Professional financial planners often utilize whole life insurance cash value as a “volatility buffer” or a personal bank. In years when the equity markets are down, a retiree can draw from their policy’s cash value for income rather than selling stocks at a loss, giving their portfolio time to recover. This is often referred to as a “buffer asset” strategy.

Additionally, the “Infinite Banking Concept” or “Bank On Yourself” methodology involves using policy loans to finance large purchases like vehicles, equipment, or real estate. By borrowing against the policy instead of using a traditional bank, the individual retains control over the repayment terms and continues to build equity within their own financial ecosystem.

Considerations and Limitations

While the benefits are substantial, whole life insurance is not without its drawbacks. The primary concern is the high cost of premiums compared to term insurance. For a whole life policy to be effective, the policyholder must have the cash flow to sustain the premiums over the long term. Surrendering the policy in the early years usually results in a net loss, as the surrender charges and initial fees may exceed the accumulated cash value. Furthermore, whole life insurance should not be viewed as a high-growth investment like the S&P 500; rather, it is a low-volatility, fixed-income alternative that provides a unique blend of safety, liquidity, and tax benefits.

Conclusion

Whole life insurance cash value represents a sophisticated intersection of protection and wealth management. By providing a guaranteed rate of return, potential for dividends, and significant tax advantages, it serves as a foundational asset for those looking to secure their family’s future while maintaining access to capital today. While it requires a long-term commitment and careful planning, the ability to accumulate a tax-advantaged pool of capital that is uncorrelated with market fluctuations makes it a valuable component of a diversified financial portfolio. As with any complex financial product, consulting with a qualified insurance professional or tax advisor is recommended to ensure the policy is structured correctly to meet specific financial objectives.