HSA vs. PPO Health Plans: A Comprehensive Guide to Selecting the Optimal Coverage

Introduction to Modern Health Insurance Selection

Choosing a health insurance plan is one of the most critical financial decisions an individual or family can make annually. As healthcare costs continue to outpace inflation, understanding the structural differences between a Health Savings Account (HSA)-qualified High Deductible Health Plan (HDHP) and a Preferred Provider Organization (PPO) plan is essential. While both provide a safety net for medical expenses, they operate on fundamentally different financial philosophies. This guide provides a deep-dive analysis into the mechanics, advantages, and drawbacks of HSA vs. PPO plans to help you make an informed decision.

Understanding the PPO (Preferred Provider Organization)

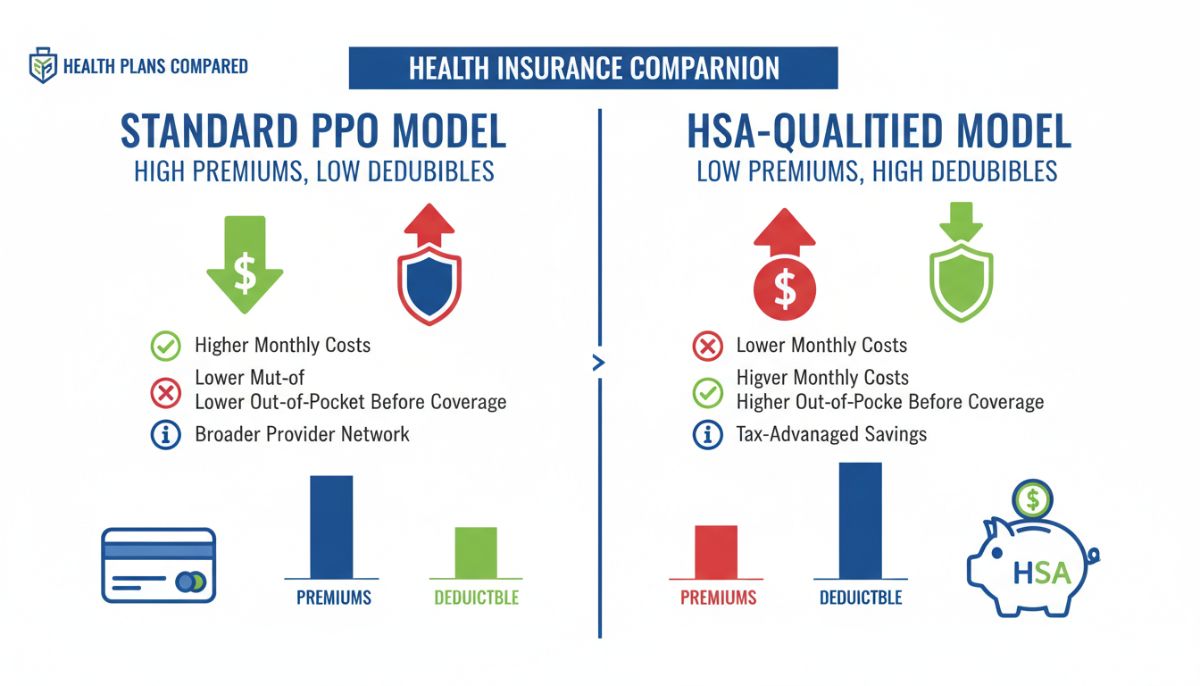

A PPO plan is often described as the ‘traditional’ choice. It is characterized by higher monthly premiums but lower out-of-pocket costs at the point of care. One of the primary attractions of a PPO is its flexibility. Participants are encouraged to use a network of preferred providers, but they also have the freedom to see specialists or out-of-network doctors without a referral, albeit at a higher cost share.

In a PPO, the deductible—the amount you pay before the insurance company begins to cover costs—is typically lower than that of an HDHP. Furthermore, PPOs often use a ‘copayment’ structure, where you pay a flat fee (e.g., $25 or $50) for a doctor’s visit or prescription even before the deductible is met. This predictability makes PPOs highly attractive to individuals with chronic conditions or families who require frequent medical interactions.

Understanding the HSA-Qualified HDHP

The HSA-qualified plan is built around a High Deductible Health Plan (HDHP). As the name suggests, the deductible is significantly higher than that of a PPO. You are responsible for 100% of your non-preventive medical costs until that deductible is reached. To offset this high initial cost, HDHPs offer much lower monthly premiums, effectively shifting the responsibility of managing healthcare funds from the insurer to the consumer.

The defining feature of this arrangement is the Health Savings Account (HSA). An HSA is a tax-advantaged savings account available only to those enrolled in an HDHP. The funds in this account are intended to cover the high deductible and other qualified medical expenses. Unlike a Flexible Spending Account (FSA), HSA funds do not expire; they roll over year after year and remain with the individual even if they change jobs or retire.

The Triple Tax Advantage of the HSA

For many high-income earners and savvy investors, the HSA is viewed as much as an investment vehicle as it is a healthcare tool. This is due to its unique ‘triple tax advantage’:

1. Tax-Deductible Contributions: Contributions made to an HSA are either pre-tax (via payroll deduction) or tax-deductible on your federal income tax return, reducing your overall taxable income.

2. Tax-Free Growth: Any interest or investment earnings on the funds within the HSA grow tax-free.

3. Tax-Free Withdrawals: Withdrawals for qualified medical expenses are not taxed.

Comparative Analysis: Premiums vs. Deductibles

The fundamental trade-off between HSA-qualified plans and PPOs is the ‘Premium vs. Out-of-Pocket’ balance.

With a PPO, you are essentially ‘pre-paying’ for your healthcare through high monthly premiums. This reduces the financial shock of a sudden illness or injury. For a person who visits the doctor ten times a year, the total cost of premiums plus copays in a PPO may be lower than the total cost of an HDHP where the deductible is never fully met.

Conversely, with an HDHP, you save money every month on premiums. If you are generally healthy and only require preventive care (which is covered 100% by both plans under the Affordable Care Act), those premium savings can be deposited directly into your HSA. Over several years, a healthy individual can accumulate a significant ‘medical war chest’ that can be used for future major expenses or even as a supplement to retirement savings after age 65.

Evaluating Your Healthcare Consumption Profile

To choose the right plan, you must audit your medical history and future expectations.

The PPO is likely better if:

- You have a chronic condition requiring regular medication and specialist visits.

- You are planning a major medical event, such as surgery or having a child, in the upcoming year.

- You prefer financial predictability and do not want to worry about a $3,000 or $5,000 bill for an unexpected ER visit.

- You value the widest possible choice of doctors without administrative hurdles.

- You are generally healthy and rarely visit the doctor.

- You have the financial discipline to save the premium difference into the HSA.

- You have an emergency fund capable of covering the full out-of-pocket maximum if a catastrophe occurs.

- You are looking for a long-term, tax-advantaged investment vehicle.

The HSA/HDHP is likely better if:

The Role of the Out-of-Pocket Maximum

One common misconception is that an HDHP is ‘riskier’ than a PPO. While it feels riskier because of the higher deductible, both plans have an ‘Out-of-Pocket Maximum.’ This is the absolute most you will pay in a calendar year for covered in-network services. In some cases, the out-of-pocket maximum for an HDHP is comparable to that of a PPO. When you factor in the premium savings of the HDHP, the ‘worst-case scenario’ (a major accident or illness) can actually be cheaper under an HDHP than a PPO.

Conclusion: A Strategic Decision

There is no universal ‘best’ plan; there is only the plan that best aligns with your health needs and financial strategy. The PPO offers peace of mind through lower deductibles and higher flexibility, making it the gold standard for those with high medical utilization. The HSA-qualified HDHP, however, offers unparalleled tax benefits and lower fixed costs, making it a powerful tool for those who are healthy or looking to maximize their long-term wealth.

Before enrolling, carefully calculate your ‘total cost of ownership’ for both plans: (Annual Premium) + (Expected Out-of-Pocket Costs) – (Tax Savings/HSA Contributions). By looking at the hard numbers and your health history, you can move forward with confidence in your healthcare coverage.